This post is part of a series of informational posts on current topics. Today we look at Open Banking and the new digital banks – what they are, how they work, and what implications they hold for the future.

“Open banking” and “digital banking” as concepts have been around a good while now, but many people even in financial services are not clear on their meanings.

Here is what the terms actually mean:

Open Banking refers to the various initiatives around the world of implementing data sharing between banks and third parties.

Digital Banking refers to the new types of bank that offer banking services without physical branch infrastructures and without using legacy banking systems. Digital banks are also known as new banks, challenger banks, or the preferred industry term “neobanks”.

So let’s look at these two concepts one at a time.

Open Banking

Open Banking is the concept of sharing banking data between banks and third parties. Drivers of Open Banking are the desire of governments and regulators to give customers more control over their data; to encourage competition and innovation in banking services; to modernise the banking industry; and to facilitate connectivity and data movement between entities.

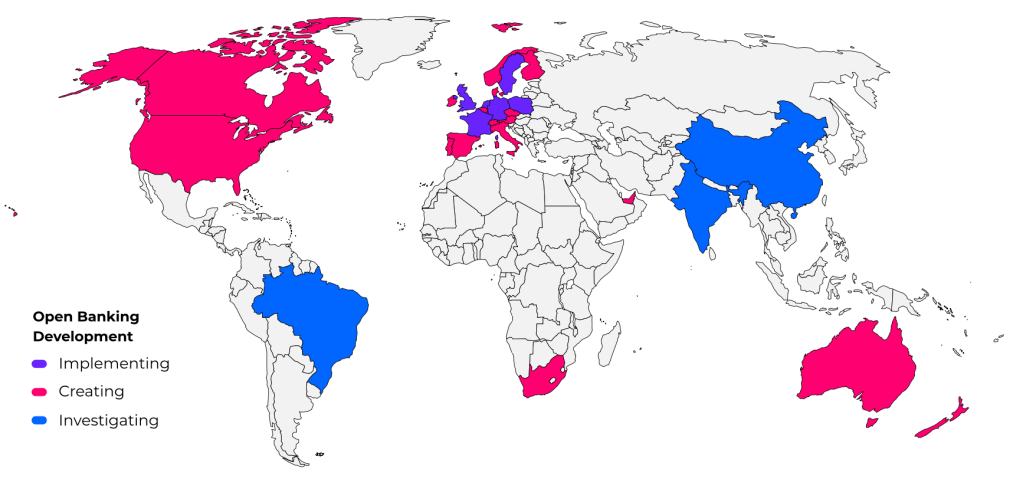

Open Banking is growing around the world. First to implement was the UK in 2018, and since then the US, EU, India, Japan, South Korea and Australia have begun to roll out their own versions. Different jurisdictions are implementing open banking differently; the UK, Hong Kong and Australia are very much regulation-led, while the US, India, Japan and South Korea are more market-led in their approach. But all share some commonalities.

Common elements in Open Banking regimes worldwide: - promoting, enabling and accelerating data sharing - API-based - regulated, to varying extents

In Australia, Open Banking is the first wave of the Consumer Data Right (CDR), which begins with banking and will subsequently be applied to Energy and Telecom – and potentially other sectors in future.

What does Open Banking mean in Australia?

It refers to data, not banking services (though Open Banking does have the potential to open up the types of service that can be offered to consumers of banking services).

The governing framework is the Consumer Data Right (CDR). CDR allows customers to easily share their bank data with other banks or third parties.

Anticipated uses of Open Banking in Australia

- Budgeting Apps such as Frollo or others, can use the Open Banking API to get data more securely, more reliably and faster than by screen-scraping.

- Switching: A big intended consumer benefit of open banking is to make it easier for consumers to switch banks. Customers considering switching banks could give their new bank access to their current banking data to provide a customised quote, pre-fill their automated payment setups, and make switching faster with less friction.

- Lending and credit scores: Customers applying for loans or checking their credit scores can give (or may be asked to give) lenders their bank data for faster more accurate assessment.

- Platform aggregators such as wealth platforms and advisory reporting services can aggregate a client’s accounts and transactions from multiple banks for consolidated reporting and wealth management.

Other uses are expected to evolve. In addition, companies that get in early can position themselves as consultants or technology sellers to others.

What data is available?

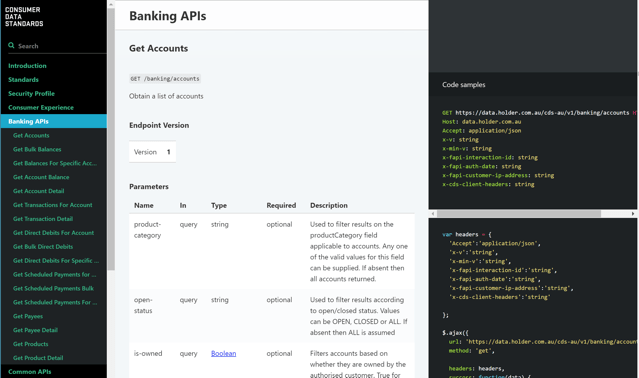

CDR has made available Product, Customer, Account, Balances and Transaction data. The data protocol is the Consumer Data Standards, the governing framework of which is the CSIRO’s Data61.

Open Banking framework

| Regulator | Australian Competition and Consumer Commission (ACCC) |

| Governing framework | Consumer Data Right (CDR) |

| Data Standards Body | Treasury, ACCC, Office of the Australian Information Commissioner (OAIC), Data61 |

| Data Standard | Consumer Data Standards – Open Banking APIs |

| Data Holders | Banks |

| Data Recipients | Non-Bank financial services providers, Fintechs |

Accreditation and Consent

Authorised Deposit-taking Institutions (banks) must become accredited as Data Holders, and entities that want to collect and use data must become Accredited Data Recipients. Accreditation is not automatic for any entity. To date, there are still very few registered accredited providers! But, as at 1 July there were a further 39 entities who had started the process to become accredited.

The consent requirement is central to Consumer Data Right. An Accredited Data Recipient (ADR) must have consumer consent to collect and make use of specified data, for a specified purpose, for a specified time. Concurrent Consent allows a Data Holder to simultaneously have multiple data sharing arrangements with an individual consumer. Consent arrangements must be easy to understand and a consumer must be able to withdraw at any time. ACCC recommends that Data Holders put in place dashboards where customers can review their data sharing arrangements.

Australia’s Open Banking Timeline

Roll-out is phased as visualised below, with the order of rollout being product data followed by account and transaction data, major banks followed by other banks and then Fintechs, and Phase 1, 2 and 3 products in order.

How do banks see Open Banking?

It is probably fair to say that the “big four” banks in Australia did not jump enthusiastically on board the Open Banking implementation. No doubt there were many in these organisations who were keen, but legacy systems, compliance and control concerns and the desire not to give up data control too early have kept the banks’ progress slow.

| Threats | Opportunities |

|---|---|

| Banks are forced to make data available to third parties including competitors | Banks can start offering new offerings and services |

| Traditional banks have a lot of work to do to make their data available via API | A chance to kick-start long-planned modernization of infrastructure and vision |

| Open Banking will make it easier for their customers to switch banks | Open Banking will make it easier for other banks’ customers to switch banks |

Which leads us on to those banks that have more enthusiastically embraced Open Banking: the digital banks, otherwise known as neobanks.

Neobanks

First, some bank context. In Australia, Authorised Deposit-taking Institutions (ADIs) – i.e., banks – are regulated primarily by APRA and ASIC, but also in various capacities by the RBA, Treasury, ACCC, ATO and AUSTRAC.

Australian banking has long been dominated by the “big four”: NAB, Westpac, CBA and ANZ.

Other banks can be thought of as falling into two broad categories: smaller banks and credit unions on legacy banking systems, some of which are subsidiaries of the big four (e.g., Bankwest as a subsidiary of CBA); and digital banks, otherwise known as new banks, challenger banks or neobanks.

“Like the name suggests, a digital bank operates digitally, usually from an app, rather than from a physical branch or office. A digital bank is a fairly loose term; the correct industry name for these banks is a neobank.

A neobank is a completely digital bank that doesn’t use any existing legacy systems to operate. This means the bank doesn’t use any physical infrastructure or digital operating systems that are already being used by existing financial institutions in Australia. The technology used by these neobanks is developed from scratch. It’s a bank that operates via an app on your phone.”

Finder, Digital Banks

In Australia, some digital banks are: volt bank, Judo Bank, Xinja, 86 400 and Up (backed by Adelaide and Bendigo Bank).

ME Bank, ING and Ubank are not “digital banks”, because they use pre-existing bank infrastructure.

Importantly, neobanks are still ADIs and are subject to all the same regulations and requirements as other banks. Deposits up to $250k in neobanks are government guaranteed just as they are in traditional banks.

Under the hood of course, the banks are very different.

| Advantages for Neobanks | Challenges for Neobanks |

|---|---|

| Can ‘leapfrog’ – start with pure digital, unencumbered by legacy technology | Customers are still slow to switch banks (Open Banking is too new and incomplete to have made a difference yet) |

| Cultural difference – dynamic, new; can attract staff; startup mindset | They have to build customer trust without history |

| Can start small – fewer staff, no branches | Offering niche or limited services limits their potential customer base |

| Flexibility – can be niche, offering limited services up to full-service banking |

The look and feel of neobanks is certainly different. A quick look at their websites and marketing campaigns highlights immediately their cultural and service differences compared to the big four banks.

We’re still in the early stages of Open Banking and digital banking in Australia. All the growth is yet to come. We haven’t yet seen all the ways the technology will be used and what services will evolve.

Bonus Round: some other banking topics

Real-time banking

The Reserve Bank has been telling banks to implement real-time payments for some time now, and has not been happy with banks’ failure to take up the New Payments Platform rolled out in 2018. BPAY has recently rolled out its OSKO payment service, which allows customers to make same-day payments to a $30,000 limit.

Peer to Peer lending

Peer to Peer lending exists in Australia but is regulated as an investment product (as it carries risk), not a banking service. It is regulated by ASIC under the AFSL regime.

Afterpay

Afterpay is an interesting non-bank financial service. It is built on an existing ‘sold debtors’ model but with the innovation that it is consumer-facing. Effectively Afterpay buys ‘accounts receivable’ from an online retailer at a discount, then recovers the debt from the customer. If you’re wondering, as I was, how Afterpay covers its default and late payment risk, the answer is this: While the interest rate on Afterpay is a lot lower for consumers than the rate offered by credit cards, due to the very short loan periods Afterpay has very high cash turnover. The compound interest on all that quickly turned over cash means that Afterpay earns an effective annual interest rate of 30% – more than enough to cover the risk of some defaults. Whether Afterpay can maintain its dominance over time or whether consumers or retailers will eventually force a change in the model, will be interesting to see.

Blockchain

Distributed Ledger Technology (DLT) is likely to disrupt digital banking further – once banks and regulators work out how to manage it. For the moment “De-Fi”, or decentralised finance, is a small but very fast-growing sector in cryptocurrency, but banks are starting to take part. ANZ is one of 75 global banks participating in blockchain trials currently.

The end of cheques

Originally planned by the Reserve Bank to be phased out by 2018, cheques still exist. The rise of digital banking will surely accelerate the final disappearance of cheques. Sometime.

The end of cash?

There are plenty of people who predict the end of cash, but I’m not one of them. The Covid-19 pandemic has certainly accelerated the average banking consumer’s shift to total digital money handling, with many of us not having carried physical cash in our wallets for months. Before the pandemic, ‘tap and go’ payments, Apple Pay, Google Pay, metro transit cards (physical and virtual) and the fast-dropping costs to retailers of non-cash payments, had all contributed to a decline in the use of cash. Even before the pandemic, we had started to see some small businesses like cafes doing away with cash registers altogether and operating completely cashless with just a payment terminal and an iPad for inventory.

Over the years, governments world-wide have cracked down on black market economies and invisible (cash) transactions, but there is a difference between reducing tax evasion and completely removing personal cash transactions.

Getting rid of cash is not by any means inevitable or easy.

Unlike cheques, it is not possible to remove cash without removing access to money to non-banked consumers. There are still many people who don’t have bank accounts.

Cash is useful for children and others who cannot manage debit cards. And what of people without internet at home or mobile phones? What of homeless people?

It is also not clear whether businesses can legally refuse to accept cash. This has been a constitutional debate in the US for some time, but the same questions have been asked in every country considering this question.

There will be push-back against cancelling cash on the basis of individual freedoms and privacy. These arguments may well eventually fall away as digital evolution overtakes them, but in the current era and especially now, where the pandemic has fuelled conspiracy theories and anti-government sentiment, that push-back would be stronger than ever.

The end of privacy?

Well… the end of lying on your finance applications is probably already here. And in general of course, the more we do digitally the less guaranteed privacy there is. Regulation is doing its best to protect consumer privacy, but… digital evolution does have its costs.

References

Open Banking

- https://www2.deloitte.com/au/en/pages/financial-services/articles/open-banking.html

- https://australianfintech.com.au/open-banking-framework-drive-customer-choice-innovation-across-australia/

- https://frollo.com.au/open-banking/

- Consumer Data Right: https://www.cdr.gov.au/

- Consumer Data Standards: https://consumerdatastandardsaustralia.github.io/standards/#introduction

Digital banks

- https://which-50.com/cover-story-australias-first-ten-open-banking-pioneers-revealed/

- https://www.finder.com.au/digital-banks

Regulation

- Banking Regulation in Australia Overview: https://uk.practicallaw.thomsonreuters.com/w-006-9098?transitionType=Default&contextData=(sc.Default)&firstPage=true

- APRA licensing FAQ: https://www.apra.gov.au/apras-licensing-process-frequently-asked-questions

- Consumer Data Right, ACCC: https://www.accc.gov.au/focus-areas/consumer-data-right-cdr-0

Other

- P2P Lending: https://moneysmart.gov.au/managed-funds-and-etfs/peer-to-peer-lending

- Blockchain and digital banking: https://www.fintechnews.org/blockchain-technology-disrupting-digital-banking/

- De-Fi: https://theconversation.com/what-is-defi-and-why-is-it-the-hottest-ticket-in-cryptocurrencies-144883

- Afterpay: https://theconversation.com/explainer-how-lending-startups-like-afterpay-make-their-money-86477